How to Reduce Chargebacks: 41 Best Tips & Techniques

-

- August 23, 2018

- 9 minutes

A strategy to reduce chargebacks will include several different tactics and tools, implemented at various stages of the transaction lifecycle.

No two strategies will be identical. Which tools and tactics are best for your business? You’ll want to test different strategies until you find the best ROI (return on investment).

Read all the tips below or choose the category you are most interested in:

Update your product offerings.

If you want to reduce chargebacks, start with the very foundation of your business — the products you sell.

1. Sell high-quality items. Low-quality and counterfeit merchandise are easy targets for “not as described” and “defective merchandise” chargebacks.

2. Clearly set expectations. Let customers know exactly what they are getting. Include every detail you can, including size, materials, colors, quantity, etc.

3. Be cautious of custom orders. It’s easy to disappoint customers with personalized orders. Maybe the customer forgot to share certain desires or didn’t realize how the final product would really look. And, unique, one-of-a-kind items usually come with a “no return” policy since the merchandise can’t be resold. These two things combined can lead to an influx of “not as described” chargebacks.

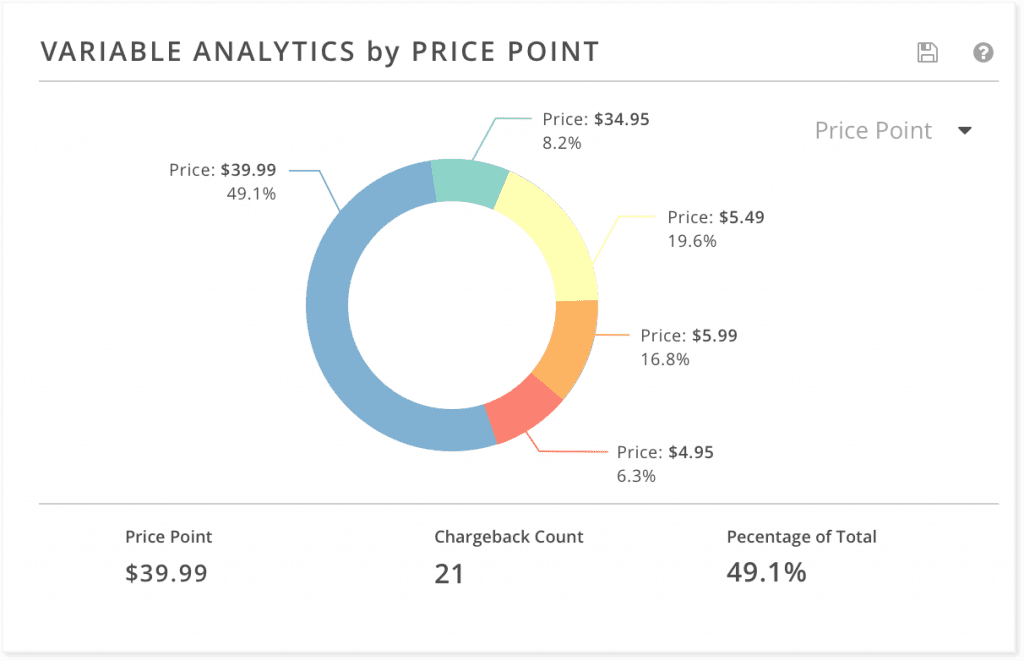

4. Find the “sweet spot” for product prices. Run A/B tests to determine which price points are most likely to initiate chargebacks. Pick prices that provide sufficient revenue, but reduce chargebacks.

5. Drop products that generate more risk than revenue. Determine which products are receiving the most chargebacks. You can do this by analyzing chargeback data by product type.

Check your marketing strategies.

Merchants often overlook marketing tactics when they build a strategy to reduce chargebacks. But if you want comprehensive protection, you can’t leave anything out.

6. Comply with marketing best practices. Check to make sure your marketing efforts aren’t unknowingly causing chargebacks. Don’t engage in bait-and-switch tactics. Don’t hide important details in the fine print. Don’t overpromise. For a complete listing of dos and don’ts, check with the FTC.

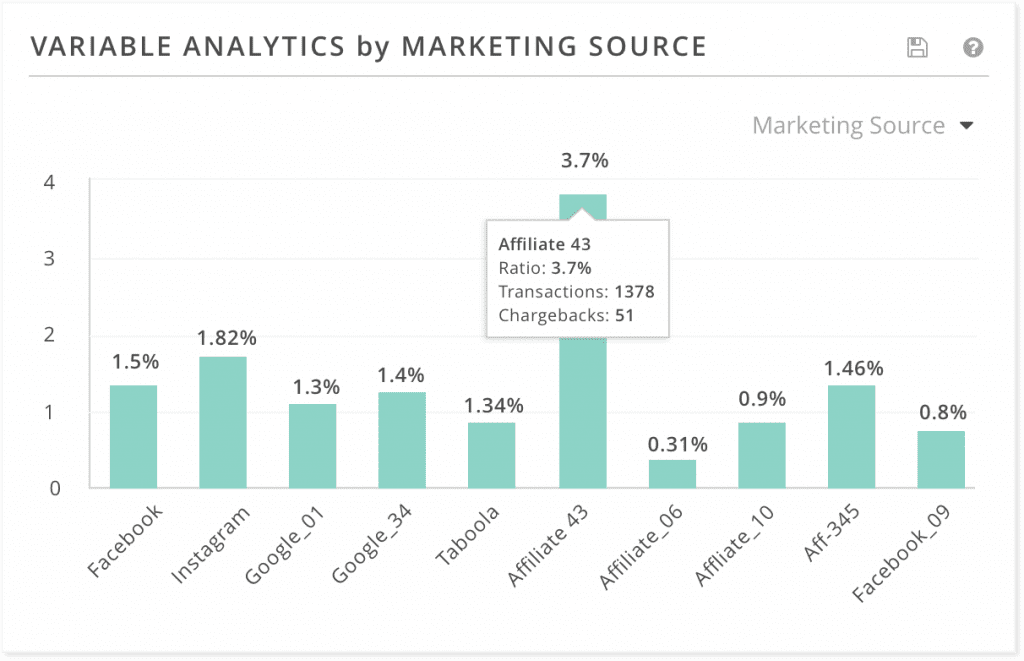

7. Replace high-risk marketing sources with target-rich sources. Learn which marketing sources are generating the most chargebacks. Focus your marketing dollars on the sources that have the highest profitability and eliminate the sources that have the high chargeback ratios.

Comply with region-specific regulations.

If you sell to a global marketplace, your efforts to reduce chargebacks will need to be more extensive than if you have a domestic-only sales structure.

8. Don’t automatically process transactions with Dynamic Currency Conversion (DCC). All transactions must be processed in the local (merchant’s) currency unless the cardholder specifically chooses to use Dynamic Currency Conversion. DCC gives cardholders the option to process a transaction in the issuing bank’s currency instead of the merchant’s currency. However, DCC usually comes with additional fees for the cardholder. If you use DCC without giving the cardholder the option to pay in the local currency, you could receive “incorrect currency” chargebacks.

9. Determine which issuing banks are generating the most chargebacks. You can do this by analyzing chargeback data by bank identification number (BIN). Funnel this information into pre-sale transaction scrubbing and chargeback representment fight rules.

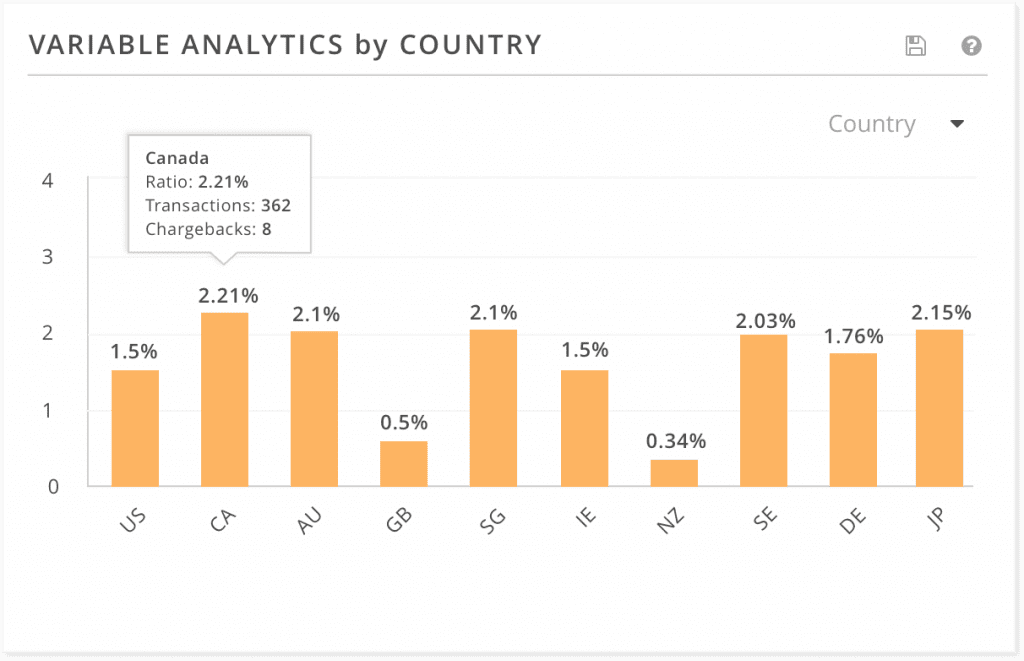

10. Evaluate risk vs. revenue on a country-by-country basis. Monitor the risks associated with each country as you add new markets. You can do this by analyzing chargeback data by country.

Use pre-sale tools.

Certain tools do more than just deflect fraud; they reduce chargebacks too.

11. Use Address Verification Service. AVS helps determine if the shopper is, in fact, the cardholder or if the card is being used fraudulently. If the AVS results reveal a high likelihood of fraud, you can cancel the order and avoid a chargeback. Also, if you use AVS during checkout, Visa could assign liability to the issuer — instead of you — for certain fraud claims. Check this article to learn why.

12. Ask for the card security code. Asking for the card security code (referred to as CID, CVV2, CVC, etc.) helps ensure the shopper is in possession of the card during checkout. A mismatch could indicate the transaction is fraudulent and needs to be cancelled to reduce the risk of a chargeback. Like AVS, requesting the CVV2 during checkout could mean you’ll reduce chargebacks resulting from fraud claims.

13. Consider using 3D Secure 2.0. 3DS 2.0 can help further ensure the cardholder is making the purchase. If you use Visa Secure, you could receive fewer allocation disputes.

Use billing best practices.

There are steps you can take before and after processing a payment to reduce chargebacks.

14. Test your billing descriptors. A billing descriptor is the short explanation of the transaction that appears on the cardholder’s statement. Descriptors play an important role in your effort to reduce chargebacks. If cardholders don’t recognize your descriptor, they might suspect fraud. Run several test purchases using different card types (Mastercard, Visa, debit, credit) to check how your descriptor displays. Consider these things while you are testing:

- For most processors, the default setting for your descriptor is your legal business name. If your legal name is different from your “doing business name,” ask your processor to replace your legal name with something your customers are familiar with.

- The length of the descriptor will depend on the issuing bank. Some issuers will truncate the descriptor so the full message won’t be displayed. This can cause confusion. Descriptors can be anywhere from 20-25 letters. If those last couple of letters are important, try abbreviations so more of your message will be conveyed.

- Depending on the length of your business name, your descriptor could also include your business phone number. This helps increase the odds the customer will contact you with issues instead of the bank. Make sure the phone number you have listed is operational and someone answers 24/7.

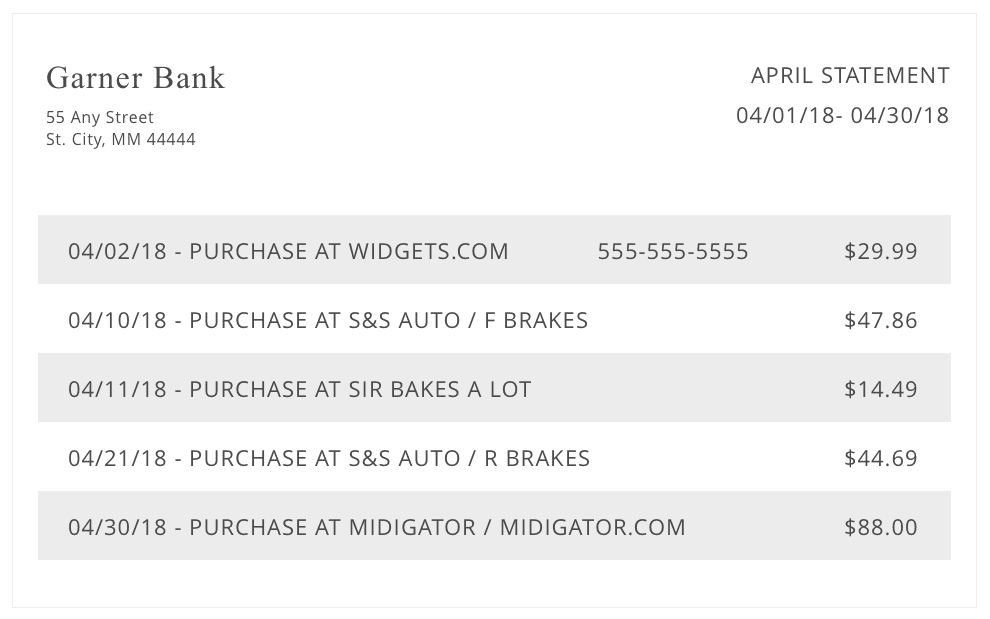

- Ask your processor if dynamic descriptors are an option. A dynamic descriptor will include your standard descriptor, followed by additional, transaction-specific information. For example, a descriptor would be “S&S Auto”. A dynamic descriptor would be “S&S Auto/FordTransmission”.

- Descriptors are set on a per-MID basis. Each merchant account will have its own descriptor. If you need to make changes, contact your processor and have your merchant account identification number ready.

15. Don’t charge the card until you are ready to ship the merchandise. The greater the amount of time between payment and receipt of merchandise, the greater the risk of a chargeback.

16. Update card-on-file information. If you allow merchants to store card information or if you use a recurring billing model, you’ll want to make sure account information is up-to-date before charging the card again. Otherwise, there is a chance transactions can clear with invalid account numbers. In these cases, you may receive an authorization-related dispute. Visa Account Updater and Mastercard Automatic Billing Updater will replace your outdated cardholder information with new data when you process the next transaction.

17. Remind customers of recurring payments before charging the card. If you charge customers on a quarterly or annual billing cycle, they may forget about the upcoming payment. Or, they might not recognize it on their statement. Notifying customers before charging the card could reduce chargebacks and doesn’t necessarily mean you’ll lose the sale.

18. Fulfill refund requests promptly. If you take too long to issue a refund, the cardholder could get impatient and request a chargeback. You’ll damage your chargeback-to-transaction ratio and have to pay the chargeback fee — when a chargeback was easily avoidable.

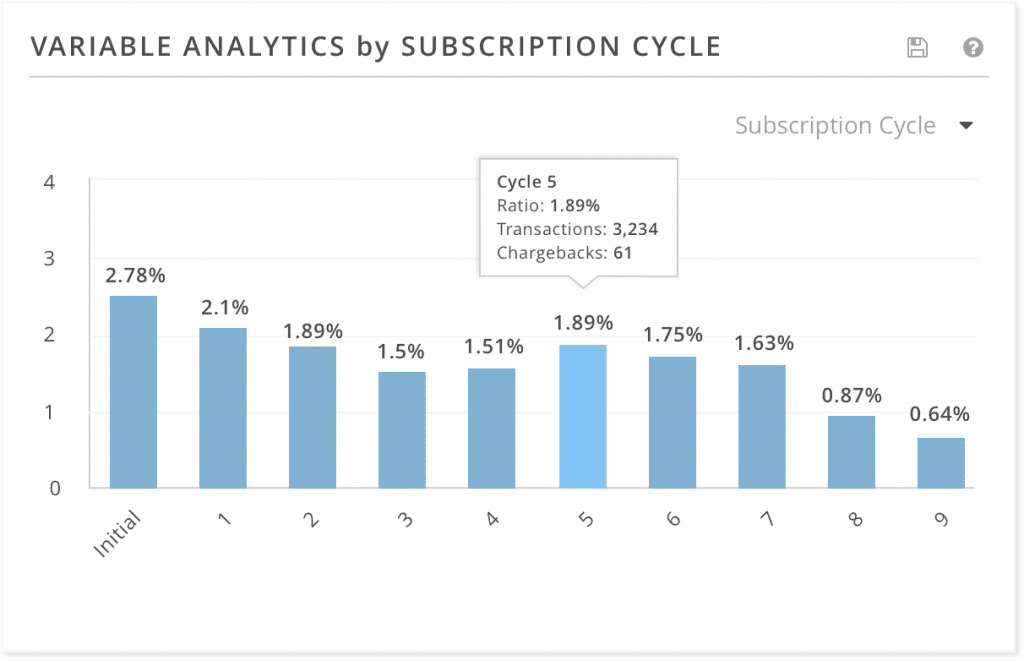

19. Act preemptively. If you use a recurring billing model, analyze chargeback data by billing cycle. Figure out which cycle is most likely to trigger chargebacks. Then, act preemptively. Reach out and inquire about satisfaction. Send a free gift. Do whatever you can to get the customer excited about your products or services again.

Conduct manual reviews.

Manual reviews are a labor-intensive process, but with the right insight, you can make data-driven decisions that help reduce chargebacks.

20. Follow up on irregular orders placed by regular customers. Suppose a regular customer has ordered two packs of diapers every month for a year. But all of a sudden, you get an order for 10 packs of diapers. Your customer might just be stocking up — or it could be a mistake. Follow up to reduce the risk of a chargeback.

21. Follow up on repeat orders or multiple purchases of the same item. Criminals will often buy items in bulk for easier resell, or they’ll make a second purchase if the first goes undetected. Or, a cardholder’s kid might buy 100 lives in their favorite online game. Regardless of who you think the potential fraudster is, you should check up on anything that seems suspicious. If you want to automate this task, see if your fraud deflection tool or processor conducts velocity checks.

22. Keep a close eye on low-dollar merchandise. Criminals often “run” a card — they make small purchases that will hopefully go unnoticed so they can determine if a card is still valid. These test purchases will result in chargebacks.

23. Consult a blacklist. If you keep track of customers who have previously filed a chargeback, you can act accordingly if they try to shop with you again. Accessing a collective blacklist would expand your intelligence by also alerting you if a customer has disputed a purchase with a different merchant.

Set fulfillment expectations.

Processing good orders is only half the battle. To reduce chargebacks, you have to make sure fulfillment goes smoothly too.

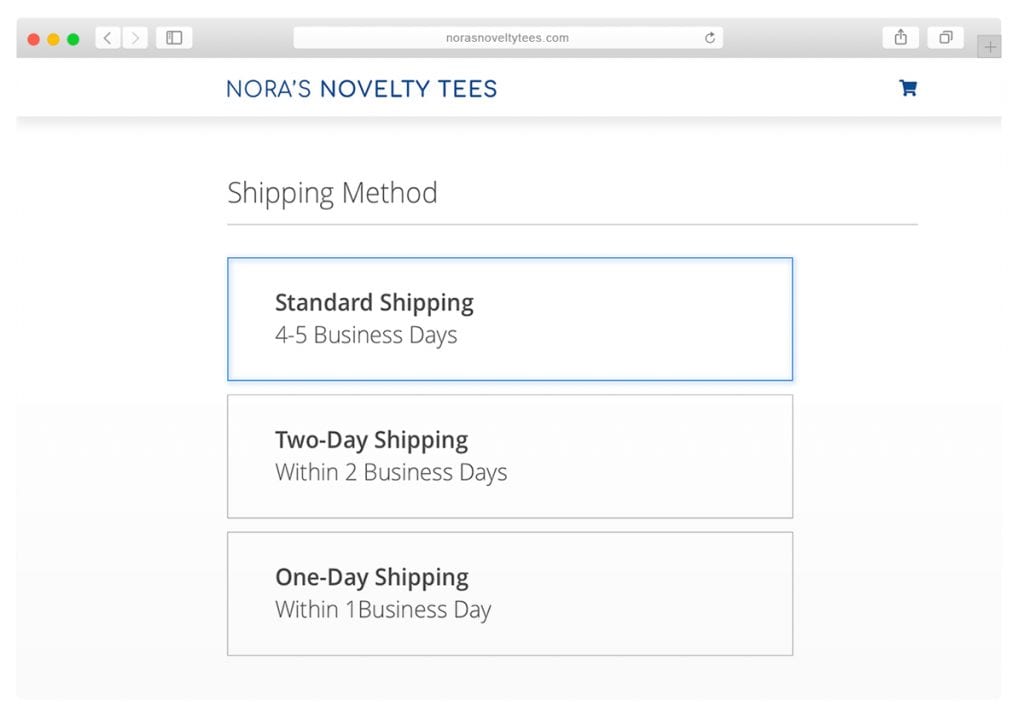

24. Offer a variety of shipping prices and speeds. Some customers will be happy to receive your merchandise whenever it arrives. But if other customers are going to demand exceptionally fast service and file chargebacks if they don’t get it, you’ll want to do your best to meet their high expectations.

25. Make sure your delivery estimates are accurate. Be honest with yourself about how long it will take to fulfill and ship orders. Chargebacks are warranted if you aren’t living up to your promises.

26. Package merchandise correctly. Use the correct size boxes and sufficient packing material so items don’t break in transit.

27. Send the correct merchandise. This seems obvious, but you’ll need to make sure your fulfillment department is familiar with your merchandise, has a complete understanding of what has been purchased, and knows what to ship.

28. Monitor inventory. Make sure your fulfillment department has a way to report low inventory. You don’t want to find out after an order has been placed that you can’t fulfill it — that’s a chargeback waiting to happen.

Check your policies.

Fair and easy-to-understand policies help reduce chargebacks.

29. Write user-friendly return and cancellation policies. The more customer-centric your policies, the more chargebacks you can avoid. Be as lenient and flexible as possible. And, make sure your policies are dynamic. For example, does your return time limit need to change from 30 days to 90 days after the holidays?

30. Make sure your policies are easy to understand. Use concise, straightforward wording. The customer needs to know exactly what is expected — both on the customer end and how you’ll respond.

31. Make your policies easy to find. Your policies need to be easily accessible at three different stages. First, customers should know what they are getting themselves into before completing the purchase. Include a link to your policy page in the product description and on the checkout page. Second, customers might want to reference the information after the purchase has been made. Include a link to the policy page in the order confirmation email. And third, customers will need access to policy information if they want a refund or cancellation. Make navigation to your policies clear and simple from the homepage.

32. Ask customers to read and agree to policies before making a purchase. Consider adding an “I have read the return policy” box to the checkout page.

Use post-sale tools.

Certain tools can be applied to cardholder disputes after the transaction has been processed to reduce chargebacks.

33. Integrate with an order validation tool. Order Insight and Consumer Clarity are powerful dispute-resolution tools. They enable merchants to communicate directly with issuers in real-time. After reviewing relevant transaction information, the issuer can hopefully clarify the transaction with the cardholder and stop a chargeback before it happens.

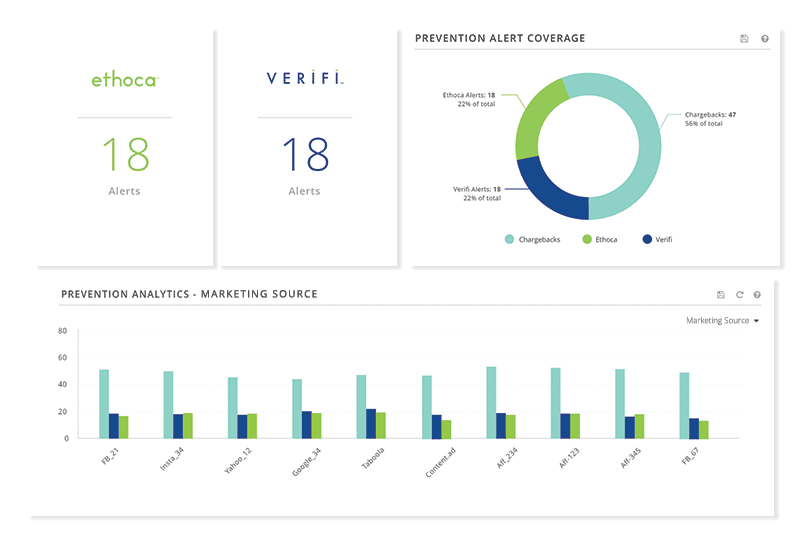

34. Use prevention alerts. Two prevention alert vendors, Ethoca™ and Verifi™, make it possible for merchants to refund transactions in real-time to resolve disputes and avoid chargebacks. Prevention alerts have the potential to reduce chargebacks significantly. However, if you want the most comprehensive protection possible, you’ll need to automate alert management.

35. Analyze prevention alert data. Prevention alerts are often issued within a couple days of the transaction, but chargebacks reach the merchant weeks or even months later. As a result, prevention alert data is a tip-off for the chargeback trends you can expect to see in the next 2-5 weeks. Analyze prevention alert data so you can identify problems earlier and resolve issues sooner.

Provide outstanding customer service.

Only a small percentage of customers contact the merchant before initiating a dispute, so it’s important that every interaction is optimized to its fullest potential to reduce chargebacks.

36. Consider offering live chat. Live chats could potentially help you “talk off” disputes in real time. Having someone answer even the simplest questions like, “Where can I find your return policy?” or, “When will my package arrive?” could resolve problems before the issue escalates to a chargeback.

37. Answer emails promptly. Numerous studies have found customers expect a response to email inquiries within one to six hours. If you fail to meet their expectations, they might file a chargeback out of spite.

38. Monitor social media. Businesses use social media for marketing. Consumers use it for communication. Be prepared to field grievances there, just like you would with any other communication channel.

39. Check call wait times. If you use a call center, ask for detailed analytics regarding call wait times. Many call centers will report the average wait time, but you need to check the longest wait time. Long wait times result in more chargebacks.

40. Share your contact information. Publish your contact information in as many places as possible—your website, email signatures, social media, etc. Eliminate the risk of chargebacks happening simply because customers don’t know how to reach you.

41. Check online review sites. If your customers are unhappy about something, you need to know about it! However, studies show you’ll only hear from 4% of dissatisfied customers. Online review sites could give you a better understanding of your customers’ true feelings and might reveal issues you didn’t know about.

Would You Like Help Managing Chargebacks?

If the processes required to reduce chargebacks seem overwhelming, Midigator® would be happy to help.

Midigator is a technology platform that prevents and fights chargebacks. We believe the challenge of running a business should be delivering great products or services, not managing payment risk. Midigator can automate your efforts to reduce chargebacks so you can focus on what matters most: growing your business.

Schedule a demo today to learn more.

Customize My Demo

Customize My Demo